Your quote is based on several common factors to give you a clear picture of the cost you can expect, though an independent agent can shop around and maybe even improve your rate!

NOTE: This quote is not final, though we did work with professional actuaries to help get you a ballpark figure to get started.

Simply put, it's a contract between you and an insurance company where you pay small monthly premiums, and upon your death, they'll pay a predetermined amount of money to whomever you choose.

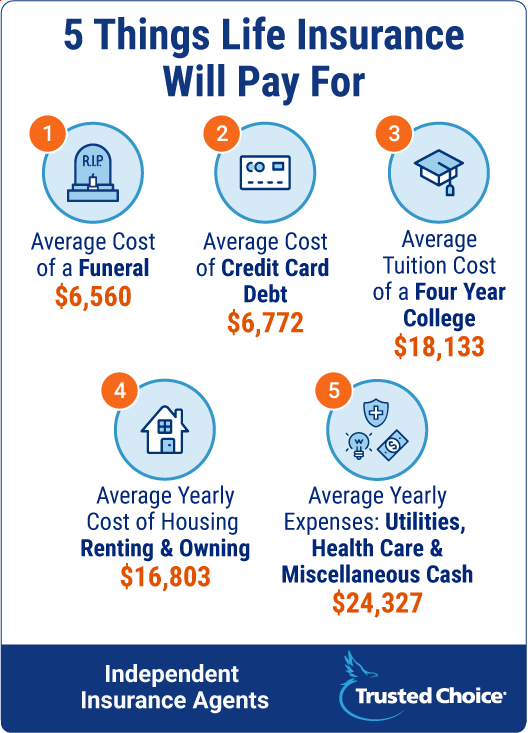

There are many different forms of life insurance, but in every case, they're designed to help protect the family you leave behind financially. Through life insurance, you can help your spouse pay off a mortgage, debt, college tuition, or just live comfortably.

The amount of life insurance needed is different for everyone. Really it all depends on your goals, your family, and the expenses your family needs to cover once you're no longer there to support them. If your plan is to just cover end-of-life expenses, you may just want funeral and burial expense insurance. But if you want to help pay off a mortgage, tuition, or other large costs, you might want something more like a term or whole life policy. A basic guideline for your life insurance limit is seven to 20 times your annual salary, but this depends on age and other circumstances.

A life insurance policy is a contractual arrangement between you and the life insurance company. The policyholder determines the amount of life insurance coverage required and pays the life insurance company a premium to keep the policy in force. If you pass away while a life insurance policy is active, the insurance company will pay out the death benefit in a lump sum to the named beneficiary.

Whole life insurance provides coverage from the day you're approved until your death. If you begin coverage when you're young and healthy, it's a very affordable option with guaranteed coverage as long as you're around. Applying for whole life in your 50s, however, is a much different, and expensive, story.

Term life insurance provides coverage at a fixed payment schedule for a predetermined period of time (usually 10, 20, or 30 years). After the period expires, the policy is terminated. This is also typically the least expensive way to purchase a substantial death benefit right when your family needs it most.

It depends. If you're in your 30s and married with young kids and a new mortgage, term life insurance may be the best option for you to help you with upcoming expenses over the next couple of decades. But if you're in your early 20s and want to plan ahead, now would be a great time to consider whole life insurance at a very reasonable price with protection that lasts your entire life. Explore our list of the 8 best life insurance companies.

The life insurance company could potentially reject the application, which could lead to you not getting coverage at all. They could also determine that there was false information on your application further down the line, and decide to cancel your coverage.

Life insurance is still included in the estate even if the proceeds are paid to a named beneficiary. So while life insurance death benefits are generally income tax free to the beneficiary, they may be subject to estate taxes.

With access to multiple insurance companies, independent insurance agents are unlike any other type of agent out there. They’ll help find you the best coverage options and most competitive prices, all for free. To find a local independent insurance agent, click here.

LIFE INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

If you don't make a plan for family members or others you'll leave behind after you pass, they could be in for a tough financial situation on top of everything else they have to handle in your absence. But that's what life insurance is for, to help protect your family by taking care of mortgages, tuition, funeral expenses, and more.

First, it's important to understand a bit more about what your choices in coverage are, and an independent insurance agent can help lay out the best options for you. For starters, though, here's a deep dive into all kinds of life insurance and which may be the right type for you.

What Is Life Insurance?

At its core, life insurance is a contract between you and an insurance company where you give them money (i.e., a premium), and if you pass away, they agree to leave a set amount of money to whomever you choose (i.e, the beneficiary). People purchase life insurance for a number of reasons, all of which are important, including to pay off college tuition, mortgages, end-of-life expenses, etc.

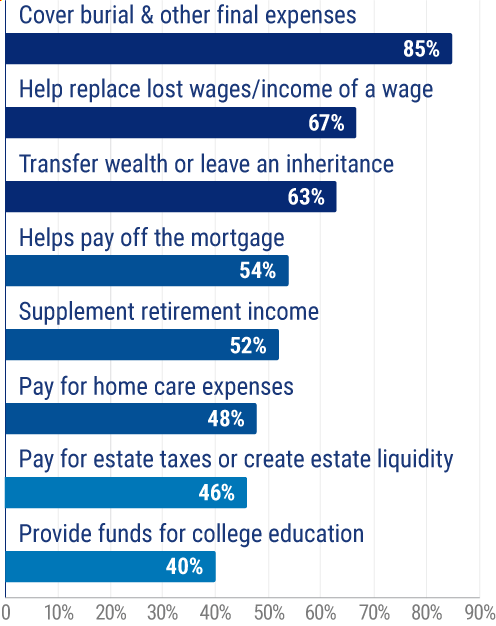

Top reasons to buy life insurance:

An independent insurance agent can help provide even more reasons life insurance is important to at least consider getting.

What Does Life Insurance Cover?

Life insurance can be used to cover all kinds of things. Your beneficiary is free to do what they want with their death benefit payout after you pass, but it's commonly used to maintain a standard of living that's similar to when you were alive and helping to provide for your family. Life insurance death benefits can also be donated to a charity of your choice if you don't have a surviving spouse or dependents.

Do I Need Life Insurance?

To understand the importance of life insurance, it's a good idea to think about the costs of life after you've passed. Consider any financial obligations your family will encounter after you're gone to dial into the perfect amount and type of coverage for you.

The right life insurance will cover most, if not all, of the biggest costs on your family's mind after you die. To determine if you need life insurance, consider if your surviving family members will be able to handle all financial responsibility on their own without your support. You may just also want to have life insurance in place to help cover your personal end-of-life expenses, such as your funeral costs.

What Are My Life Insurance Options?

The beauty of life insurance is that there's an option for most needs and budgets. Term, whole, and universal life insurance are three types of coverage that each have the same outcome, paying a set amount of money to the person of your choosing upon your death.

Term life insurance: This option is geared toward younger folks because it’s a temporary plan that only covers you for a period of time, usually 10, 20 or 30 years. If you pass away within that time frame, a set amount of money goes to the people/person you choose.

Whole life insurance: Whole life has the same concept as term, but the policy is active as long as you're alive. As an added bonus, it also has a savings account feature that accrues money, eventually hitting the policy’s coverage amount. At that point, you can cancel the policy and hold onto the cash instead, or even use your savings as a personal loan.

Universal life insurance: Like whole life insurance, a universal life policy also has a savings account feature, but the difference is a flexible premium option. These flexible premiums can be changed up or down to meet your needs.

Term life vs. whole life vs. universal life

Benefit

Term

Whole

Universal

Choose length of policy

Yes

Active for life

Active for life

Provides lifelong coverage

No

Yes

Yes

Low premium

Yes

No

No

Guaranteed payout

Yes, within term length

Yes

Yes

Accumulates cash value

No

Yes

Yes

Cash value risk

N/A

Only the insurer

Interest rate fluctuation risk

Loans / Withdrawals against benefit

N/A

Yes

Yes

Common uses

Income replacement

Income replacement / Supplemental income / Estate planning

Income replacement / Supplemental income / Estate planning

An independent insurance agent can help you determine which type of life insurance works best for you.

What Type of Life Insurance Do I Need?

To decide what type of life insurance you need, consider your current age, finances, and your future goals. You can also use our handy life insurance calculator to get a rough idea of the cost. Otherwise, check out this breakdown to help you further:

You might want term life insurance if:

You want a more affordable policy.

You want to be able to have coverage for only a set amount of time.

You have upcoming expenses you need help with in the near future.

You're young and have a family to help provide for.

You might want whole life insurance if:

You're young and healthy.

You want to have coverage that lasts your whole life.

You want to leave money behind for spouses and/or dependents.

You want the savings account feature.

You might want universal health insurance if:

You want coverage that lasts your whole life.

You want control over the size and timing of your premium payments.

You want the savings account feature that accrues interest.

You're a bit older when you apply for coverage.

If you're unsure of which type of life insurance would best meet your needs, your independent insurance agent can help you weigh your options.

How Much Is Life Insurance?

So how much does life insurance cost? Well, it depends on your policy's specifics. It also depends on your age and health status when applying for coverage. You'll generally pay much less for coverage if you're young and healthy and don't need as much coverage than if you're older and have a preexisting condition.

Here are some example premiums for life insurance:

A healthy 40-year-old female can expect to pay around $450 annually for coverage.

A healthy 25-year-old male can expect to pay around $295 annually for coverage.

A 55-year-old male smoker can expect to pay around $2,810 annually for coverage.

A terminally ill 65-year-old woman can expect to pay around $5,910 annually for coverage.

An independent insurance agent can provide you with exact life insurance quotes for your circumstances and area.

Is Life Insurance Worth It?

It's ultimately up to you to decide if life insurance is worth it. If there are any expenses your family wouldn't be able to cover themselves after your passing, life insurance may well be worth it. But for single folks with no dependents and plenty set aside in savings for their end-of-life expenses, life insurance might not make sense after all.

How to Buy Life Insurance

The process is pretty simple, really. When you work with an independent insurance agent, you're off the hook for a lot of the hard work. After you discuss your goals, they'll start the search among a number of top life insurance providers and bring the quote options to you.

Step-by-step guide to buying life insurance:

Contact an agent: Find your local independent insurance agent and discuss your goals for the future before shopping around for the best quotes.

Review quotes: Together with your agent, you'll walk through your options to find which works best for you.

Complete an application: The insurer will have you fill out an application to get a clear picture of your health, history, etc.

Take a medical exam: Most life insurance policies require you to take a medical exam before you're approved for coverage.

Sign the contract: Once you're approved, you'll sign the documents, make your first premium payment, and begin to enjoy your coverage.

As always, an independent insurance agent is your greatest ally when it comes to finding and buying the right type of life insurance for you.

Are Life Insurance Benefits Taxable?

Life insurance proceeds are generally income tax-free to the beneficiary. But proceeds may be subject to estate taxes if the insured's estate is valued at $5.5 million or higher. If you're unsure of whether your life insurance benefits are taxable, ask an independent insurance agent to review your policy with you.

Why Choose an Independent Insurance Agent?

Independent insurance agents simplify the process by shopping and comparing insurance quotes for you. Not only that, but they’ll also cut the jargon and clarify the fine print so you know exactly what you’re getting.

Independent insurance agents also have access to multiple insurance companies, ultimately finding you the best life insurance coverage, accessibility, and competitive pricing while working for you.

Best Life Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What our customers are saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.